Part 1 of this two-part series presented an optimistic picture of the future of the Ready-to-Drink cocktail category – with the spirits-based version at the center of that picture, although malt-based RTDs are in the frame as well. In this second article we’ll discuss inputs into RTD profitability.

As First Key Consulting’s George Croft points out, “The continued momentum in ready‑to‑drink beverages makes it clear that the brands winning in this category are built on strong consumer insights and reinforced by disciplined commercial fundamentals. Growth stories like Cutwater’s triple‑digit gains and BeatBox’s continued acceleration reflect sustained commitment to brand building, focused marketing, and best‑in‑class execution at retail. That same formula is playing out across the RTD landscape.”

Three high-level decisions must be analyzed by any would-be producer of RTDs, and the eventual impact on profitability is among the most important considerations in each decision. These are the choice of the alcohol base, the choice of flavors, and the choice of packaging. Of course, each of these influences’ profitability in two ways: indirectly, in how it affects consumer demand for the product; and directly, in terms of affordable materials, affordable labor, and the ability to price the product competitively.

The Choice of the Alcohol Base

The choice of base may or may not be the most important decision, but it is most likely the first one that must be addressed. The momentum would currently appear to be on the side of spirits-based RTDs. This was illustrated by the recent announcement that Mark Anthony Brands, which continues to have great success with a malt-dominant portfolio, has made “a major jump forward” for its spirits-based portfolio with the purchase of the Finnish Long Drink, a popular gin-based RTD brand.[i]

Yet current trends aside, the choice of base may be less straightforward given considerations related to distribution strategies (i.e., where you intend to sell the brand, in terms of both geography and account types) and operations (i.e., what your facility can support). Taxes and legalities of course vary by state or province, and in a given jurisdiction spirit-based RTDs may be subject to greater taxes and/or restrictions on where it can be sold. (In the U.S. the CBMA has made adding spirits to a beverage more affordable, but state regulations may essentially override it.) Many states and provinces do not allow sales of spirits in grocery stores, and direct-to-consumer sales also face varying constraints.[ii] In some cases additional licensing, or even separate facilities, may also be required.

If a brewery sorts through the above considerations and determines that a spirits-based RTD makes sense both strategically and operationally, they’ll encounter a number of ways that this option impacts profitability.

First, there’s a hidden benefit to a brewery producing a spirits-based RTD cocktail, as outlined in the First Key article Brew-Stilleries. Mixing an RTD cocktail does not tie up a tank for the time it takes for a malt-based beverage to ferment. The product can be mixed and packaged in the same day and the tank is then free to be used again. In addition, producing a cocktail mixture does not require the skills of a lead brewer. In a facility separate from the brewery, blenders could be hired to mix the RTD cocktails, saving on labor costs.

Second, a spirits base would likely allow an individual RTD brand to enjoy the halo of premiumization by justifying a higher price point. Recent industry data indicates that spirit-based RTDs continue to command a premium, with a significant share of consumers willing to pay more for them than malt-based alternatives.

In addition, a brewery may choose to partner with a spirits producer in order to take advantage of their established brand recognition and equity. Of course, the brewery would need to make a deal with the spirit producer to use their name and product. Similarly, some cocktail names are trademarked and a deal with the trademark holder would have to be made to produce the cocktail. Given the importance of authenticity in the category, being associated with a name brand or a trademarked cocktail name may well be worth the investment, especially since these are likely to command a still-higher price point.

Although growth in malt-based RTDs has recently trailed the spirits-based segment, breweries that choose malt as a base, due to distribution strategy and/or production capabilities, have other advantages and disadvantages. (See the First Key article Hard Seltzer Production Methods.)

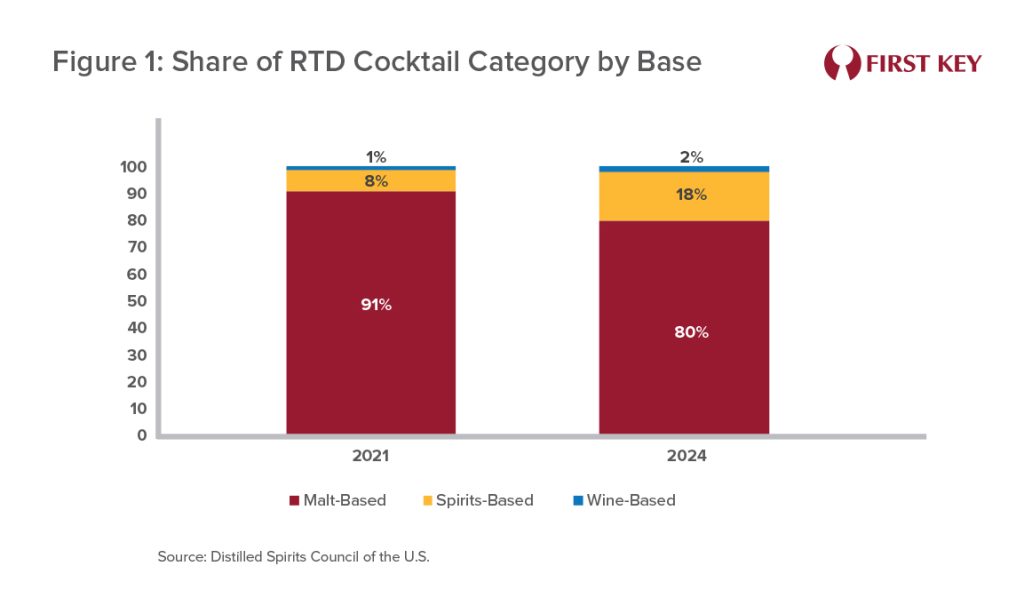

First: while the spirits-based side has the momentum, the malt-based side is far from dead. It still represents 80% of the market as shown in Figure 1 below. While piggy-backing on faster growth is frequently a sound approach, a strategy of carving out a place within a segment that’s still four times bigger can be successful in its own right.

Planned or recent introductions by a number of breweries, large and small, would seem to validate the idea that there’s still a role for new malt-based entries. Constellation has introduced Rule of Five hard punch into test markets. In September of 2025, in partnership with Sazerac, Coca-Cola’s Red Tree division announced its intention to introduce Fresca Hard, a malt-based complement to their Fresca Mixed spirits-based RTDs.[i] And each of White Claw’s new Clawtails canned cocktails proudly declares itself to be a “Premium Malt Beverage” front and center on the label.[ii]

However, among smaller brewers who’ve introduced malt-based RTDs, the experience and the takeaways have been mixed. Josh Secaer, Owner of Gambit Brewing Company in St. Paul, Minnesota, reported “[Our flavored malt beverage] is definitely a nice addition to the brewery, especially since we can’t have wine or cocktails with our licensing. We do get a lot of people that gravitate that way for reduced gluten.” On the other hand, Adam Ross, Head Brewer at Twin Span Brewing in Bettendorf, Iowa, said “Our best selling in this line is Wisconsin Juice,” which is a 10% ABV dextrose-based FMB with Door County cherries, orange puree, and (non-alcoholic) brandy extract. “It’s still pretty niche though. I’m on the fence if I would call it a success or even brew it again.”

Another potential argument for using a malt base may depend on the demographic target. The resulting lower price to the consumer may be appealing to cash-strapped Gen Zers. As Rabobank Senior Beverage Analyst Bourcard Nesin advised, “For now, companies would be well served to remember that young people are broke and, therefore, likely can’t afford that superpremium tequila.”[iii] Diageo has apparently taken heed, as their Captain Morgan Sliced line of RTDs uses malt specifically to be more accessible to “price-conscious shoppers.”[iv]

The Choice of Flavors

Choosing the flavors of the beverage will also, of course, affect profitability. This decision should be based in large part on the target customer. Is it GenZ/Millennials, or older cocktail drinkers? Combinations of fruit flavors — or fruit flavors and other spices — have proven effective in attracting younger generations, who typically are more willing to try new products. However, recently the market seems to be headed away from “out there” combos towards “safer” known combinations of flavors. Brewers targeting Gen Z/Millennials should consider a portfolio of at least three or four flavors, if only so their single-serve products can be sold in a mix pack. These often outsell packages of one flavor only.

If targeting established cocktail drinkers, a case can be made for choosing cocktails that are more difficult to make in their traditional form – those requiring bar tools, for example. A more complicated cocktail may appeal to those consumers seeking a sense of sophistication, and they may be able to command a premium price.

But if a cocktail can be made simply, drinkers may be tempted to make it themselves. So, for example, a screwdriver — vodka with orange juice as the mixer — might not be a great choice. Still, one could argue that even a premixed screwdriver is more convenient than one hand-mixed by the drinker, and so a well-known two-ingredient mixed drink may do well in the market despite its simplicity. Case in point: the Jack Daniels and Coca-Cola RTD cocktail is Brown-Forman’s best seller. Without a corporate tie-in, however, RTD versions of simple-to-mix cocktails may not command a higher price.

The Choice of Packaging

Single-serve 12-ounce slim cans (355mL) or larger have become a staple of the category, driven by their appeal to younger drinkers and their fit with C-store purchase occasions. However, with premiumization the highest-priced spirit-based RTD cocktails may benefit from larger format glass. This may reinforce that sense of sophistication those drinkers may be seeking.

It will be no surprise to anyone in the industry that the choice of glass versus aluminum and other packaging becomes more complicated due to volatile commodity markets. Glass is made in both Canada and the US, but it is also imported from China, Mexico, and other countries. Canada is the 4th largest producer of aluminum, but it imports bauxite from other countries. Increased recycling could make both glass and aluminum more available. Only about 30% of glass waste gets recycled in Canada and the US. And while 80% of aluminum is recycled in Canada, only a little over 40% is recycled in the U.S.

The Future

Industry trends and consumer purchase behaviors indicate that the RTD cocktail category will likely continue to grow over the next five years. However, despite the favorable category dynamics, consumer preferences may shift, especially among Gen Z, as younger consumers are more open to new experiences.

But the reaction of both retailers and consumers to the inevitable further proliferation of brands, flavors, and packages[v] may be key to future development of the category, and of individual brands. First, there’s the question of how to deal with increasingly crowded shelf space. In many cases retailers may choose to address this by taking space from beer, which of course from the perspective of brewers is no solution at all. And although RTD cocktails are currently commanding prices that allow for a comfortable profit margin, competitive price cutting by some new entrants seeking a toehold in the market could erode that.

In addition, there may be challenges to supply chains as to the availability of aluminum, glass, and other materials from other countries faces potential uncertainty.

However, it remains true that the current dynamics of the RTD category sales appear to favor continuing growth. George Croft points out that, despite the fact that the ten largest brands control nearly 80% of total dollar sales “…growth remains broad-based. Nine of the top ten brands are growing, most at double- or even triple-digit rates – underscoring that RTD is far from a zero‑sum game.”

There are a large number of established cocktails to choose from and a variety of packages in which to market them. Currently, the best bet for a profitable RTD would be a spirit-based cocktail with the spirit coming from a known distiller. However, any RTD cocktail made with vodka, tequila, or rum — or even whiskey — has a good shot at finding a market while being sold at a premium price.

As Croft sums up, “Brands that are winning are doing so by pairing compelling propositions with disciplined brand building, distribution expansion, and retail execution, proving that scale and momentum in RTD are earned through fundamentals, not fads.”

In any case, as you navigate your new beverage plans and feasibility, a well-developed profitability analysis and capacity modeling can determine whether your RTD has the runway to become successful.

To learn more about profitability for your beverage brands please contact us

[i] https://www.brewbound.com/news/mark-anthony-brands-to-acquire-finnish-long-drink

[ii] For some insight into Canadian provincial regulations, see https://globalnews.ca/news/10171555/alcohol-sales-rules-by-province/; for similar information by U.S. state, see https://www.nabca.org/control-state-directory-and-info

[iii] https://www.foodbev.com/news/coca-cola-partners-with-sazerac-to-expand-alcoholic-beverage-portfolio

[iv] https://www.whiteclaw.com/products#clawtails

[v] https://media.rabobank.com/m/18086d3a9adee411/original/The-real-reasons-Generation-Z-is-drinking-less-alcohol.pdf

[vi] https://www.fastcompany.com/91140264/ready-to-drink-rtd-cocktails-gen-z-millennials-liquor-brands-flavor-innovation

[vii] https://www.theiwsr.com/insight/five-ways-the-rtd-market-in-the-us-is-changing/