For decades, beer, wine, and spirits have been viewed as the foundational pillars of the North American alcohol industry. That framework is now being challenged. Growth across all three traditional categories has slowed, even as a steady stream of alternatives such as hard seltzers, flavored malt beverages, ciders, and low‑ and no‑alcohol options have entered the market. Yet among this crowded field, one category stands apart. Ready‑to‑drink cocktails (RTDs) have emerged as the most compelling growth story in beverage alcohol today, reshaping consumer expectations and forcing the industry to rethink what the next era of alcohol looks like.

The RTD category’s strong gains are projected to continue over the remainder of this decade, with estimates of annual growth of up to 15%[i] (although forecasts vary widely by source). In the first of a two-part series, we break down the possible reasons for continued success for RTDs’ growth, which will be followed by a profitability-centered discussion on decisions related to introducing a new RTD.

The Industry is Leaning into Spirits as a Base

Spirits-based RTDs have been growing significantly faster than their brewed or wine-based siblings. Brands like Cutwater, Surfside, Sun Cruiser leading the way and other fast-growing brands such as Carbliss, Good Boy and Long Drink also growing rapidly. In 2025 data reported by DISCUS, spirits-based RTDs have more than doubled their market share since 2021 and are up 11 percentage points.[ii]. This growth continues into 2026 with confirmation in a recent Beer Business Daily piece stating, “YTD through the week ending Feb. 28, 2026, RTD Spirits dollar trends are running at +40% year-over-year in 2026 – vs the similar +36% over the last four weeks, and a lot faster than the +28% for the last 52 weeks”. While some of this growth is attributable to opportunities for more favorable tax treatment found in the Craft Beverage Modernization Act (CBMA)[iii], this growth mostly reflects a convergence of consumer demand and consumer-centric new product development now centered on RTDs using spirits as a base.

While this segment currently accounts for only about a fifth of RTD volume, 55% of surveyed RTD drinkers say they prefer spirits as a base.[iv] In a Forbes piece, NielsenIQ vice president Jon Berg stated: “Consumers have said, ‘I really want to have something that’s more authentic’… Something that tastes like a margarita should have tequila in it.”[v]

Jaime Jurado, Beverage Operations Director at Alaska Pacific Beverage Company, concurs. “Breweries which either have a full distillery (such as Alaskan Brewing) or a distillers permit and who import bulk spirit have the authenticity of having true distilled spirits in the can… I think consumers care if, say, their Moscow Mule, or Gin ‘n Juice has spirits in it instead of being a Flavored Malt Beverage (FMB).”

Yet in some cases consumers remain unclear about what their RTD is made from. Greater transparency around whether products are spirits- or malt-based will both drive and reinforce future growth in spirits-based RTDs.

With all of that said, there may be select opportunities for new malt-based RTDs as well, to be discussed in Part 2 of this two-part series. And while the remainder of Part 1 will focus on the future of spirits-based RTDs, much of the discussion could apply to the future of RTDs more generally.

Spirits-Based RTDs and Implications of the Convenience Factor

Convenience is frequently cited as a reason for rise of the RTD category more generally, and indeed, convenience is arguably contributing disproportionately to the rise of spirits-based RTDs. That’s because spirit-based formulations most closely mimic the experience of drinking a traditional cocktail, normally the most “inconvenient” alcohol beverage option in terms of preparation. Making cocktails at home can be fairly complicated; you may need shakers, strainers, or muddlers in addition to a jigger. If you’re adding fruit, you may need a cutting board, a paring knife, or a grater (or zester). You need to have all the appropriate ingredients — including bitters or flavored liqueurs — on hand and fresh (especially in the case of plant products). An RTD cocktail eliminates the need for a cocktail set and a liquor cabinet full of liqueurs.

Yet it would be oversimplifying to say that the rise of RTDs’ has been all about convenience, and in fact the convenience factor would seem to be relevant largely (or entirely) in at-home drinking occasions. (NIQ reports that 91% of RTD consumption occasions take place at home or at someone else’s home, similar to percentages reported for spirits, wine, and beer.[vi]) In a bar or restaurant, ordering a traditional mixed drink involves no more inconvenience to the drinker than does any other beverage type. Thus, the same drinker who chooses a traditional cocktail when in a bar or restaurant may well opt for an RTD, especially a spirits-based RTD, when at home.

This raises the question of whether the pandemic-related lockdowns of 2020 and 2021 gave a meaningful boost to a category whose dynamics already favored at-home consumption. This may well be true; some knowledgeable industry observers appear to take this conclusion on faith.[vii] Much has been written, in turn, about how the pandemic influenced Gen Z to become a “homebody generation,” more comfortable staying in than going out long after the pandemic wound down.[viii]

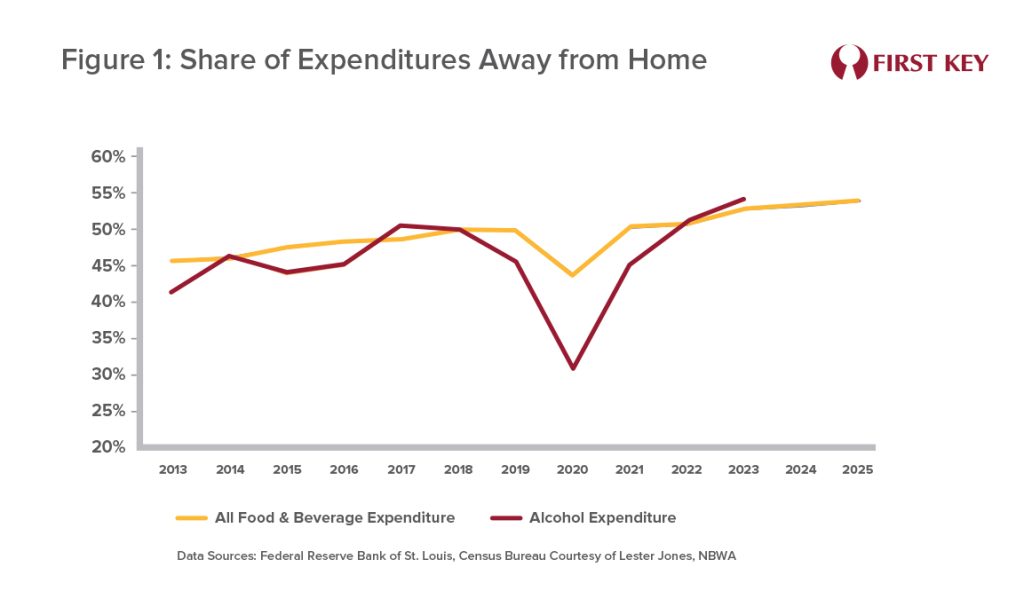

However, while there may be a significant subset of drinkers who are staying at home more often since 2020, the numbers would seem to indicate that they’re in the minority. In fact, the share of food and beverage dollars spent away from home (versus at home) returned to its long-term upward trend in 2021, immediately after the pandemic, and reached a 21st-century high in 2025. While similar splits specific to alcohol beverages are only available through 2023, Figure 1 shows that the on-premise share of beverage alcohol spending unsurprisingly parallels that of overall food and beverage spending away from home over time. As Fintech’s Eric Kiser and the NBWA’s Lester Jones wrote in a recent article, “…consumers are committed to spending money at bars, restaurants, and breweries as they prioritize social interaction.”[ix] It seems apparent that going out is back in style.

If at-home occasions favor the choice of RTDs over traditional cocktails, does this on-going return to bars and restaurants constitute a headwind to RTD growth? In all probability, any such headwind will be minor relative to the category’s forward momentum. A visual extrapolation of the trend portrayed in Figure 1 results in an estimated share of 57% in 2030 – meaningful growth, and yet not all that much more than the 54% figure in 2025. It’s unlikely this will create a significant drag on an RTD category that’s still developing, and is a long way from its full potential.

The On-Premise as Source of Opportunity

Given that at most 9% of RTD occasions currently take place in the on-premise, a new or established producer of RTDs might decide that their sales, marketing, and distribution efforts should be tailored to the off-premise. But there are also some strong arguments to be made for investing disproportionately in bars and restaurants. Not only would this be a matter of “zigging while others are zagging,” it invokes the timeless maxim that brands are built in the on-premise.

There may be no better recent confirmation that this bit of wisdom still applies, than the success of Sun Cruiser. Beer Business Daily recently reported on Boston Beer’s Q4 and full year earnings call, where CEO Jim Koch indicated the brand had “a great 2025,” growing “almost 400%” and is now “about the no. 5 RTD from kind of nowhere a year and a half ago.”[x] He added that the on-premise accounts for 40% of the brand’s volume in many markets – a result of intentional brand-building in the on-premise by means of “old school, grassroots bar-by-bar selling on the street,” including 75 brand ambassadors, sampling teams, and point-of-sale. Koch called this “an important lesson for the whole beer industry today.” If enough RTD producers heed Koch’s advice, overall category growth may well reach a new level as sales in an arguably under-developed channel strive toward their full potential.

Building on all these good reasons to believe in the future of RTDs, Part Two of this two-part series will discuss the key decisions that must be considered in developing a brand, whether new or relatively established, with a focus on what drives profitability.

To learn more about category dynamics for RTD beverages please contact us

[i] https://www.grandviewresearch.com/industry-analysis/us-ready-to-drink-cocktails-market-report

[ii] https://www.distilledspirits.org/wp-content/uploads/2025/02/FINAL-DISCUS-Annual-Economic-Briefing-Presentation-2025.pdf

[iii] https://www.ttb.gov/regulated-commodities/beverage-alcohol/cbma/craft-beverage-modernization-and-tax-reform-cbmtra

[iv] https://www.distilledspirits.org/wp-content/uploads/2022/09/Final-DISCUS-Handout-9.14.22-v2-1.pdf

[v] https://www.fastcompany.com/91140264/ready-to-drink-rtd-cocktails-gen-z-millennials-liquor-brands-flavor-innovation

[vi] https://www.bevnet.com/spirits/2023/the-five-ways-rtd-alcohol-consumption-is-changing-according-to-niq/

[vii] See, for example, https://daily.sevenfifty.com/ready-to-drink-cocktails-by-the-numbers/

[viii] https://www.bonappetit.com/story/how-bars-are-adapting-to-gen-z-the-homebody-generation?

[ix] https://www.nrn.com/beverage-trends/beer-trends-2025-social-drinking-rebounds-amid-shifting-consumer-habits

[x] https://beernet.com/bbd/bbd-article/jim-koch-calls-for-a-revival-of-brand-building-strengths/ (subscription required)